The Emergence of Mobile Money in Ethiopia and the Fourteen Years It Took Us to Catch Up

The Emergence of Mobile Money in Ethiopia and the Fourteen Years It Took Us to Catch Up

The emergence of mobile money in Ethiopia, how a country where less than 1% of people had a mobile money account in 2017 reached tens of millions of users within years of a single regulatory shift, and why the barriers holding everyday Ethiopians back are far from over.

The emergence of mobile money in Ethiopia, how a country where less than 1% of people had a mobile money account in 2017 reached tens of millions of users within years of a single regulatory shift, and why the barriers holding everyday Ethiopians back are far from over.

Essay

9

Min Read

I remember watching an Indian movie as a kid, and when I say kid, keep in mind I'm 26 now, so that was probably fifteen or sixteen years ago. In one scene, a character orders food and pays by scanning a QR code and I remember being amazed by it. You might be wondering where I'm going with this, and you're right to pause. But here's the thing: when Telebirr was introduced in 2021, a year after the National Bank of Ethiopia allowed non-bank institutions to provide digital financial services, and we finally started sending and receiving money digitally, I couldn't help but realize just how slowly our system has been catching up with the rest of the world.

According to a 2023 report by DAI Global, before 2017, only 0.3% of Ethiopians held mobile money accounts, an almost invisible figure compared to the Sub-Saharan African average of 21%. The primary bottleneck behind this gap, sustained for years, was a deeply cash-based economy dominated by state-owned financial institutions. Then in 2021, the National Bank of Ethiopia signaled a fundamental shift, opening the door to digital transformation. That same year, Ethio Telecom launched Telebirr, which quickly became the dominant force in the country's digital finance sector. That is what I want to explore in this essay: the rapid rise of digital financial platforms, the structural and institutional barriers that continue to slow them down, the distance that still separates access from true inclusion and the unfulfilled promise of digital financial services in Ethiopia and what it will take for that promise to stop being overdue.

Image from Dai Global: A person making a cash payment at a small kiosk/shop window

A System Built to Exclude

Before 2021, Ethiopia's financial landscape was defined by state dominance, structural underdevelopment, and a population with limited access to or awareness of formal financial services. Ethiopia's modern banking history traces back to 1906, when the Bank of Abyssinia was established as a foreign-owned concession, leaving the country without a single domestic financial institution. That gap was not filled until 1931, when the Bank of Ethiopia was founded under Emperor Haile Selassie. Its growth, however, was cut short by the Italian occupation of 1935–1941, which disrupted the nascent system before it could take root.

After liberation, a modest banking infrastructure began to re-emerge. When the Derg military regime seized power, all private banks were nationalized, plunging the sector into stagnation and contributing to sluggish GDP growth for nearly fifteen years.

The Benchmark: 14 Years Behind

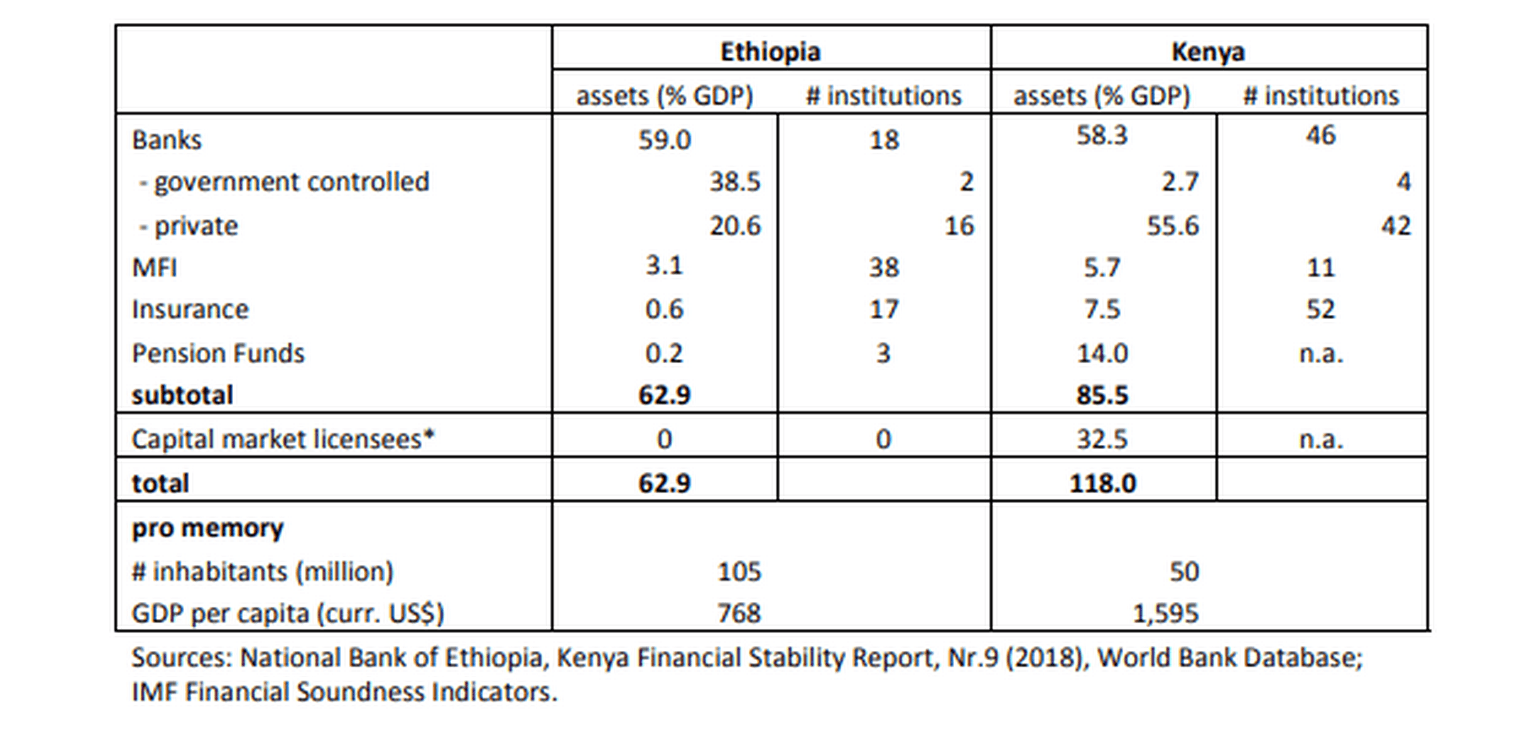

To understand the scale of Ethiopia's delayed start, consider the region. Kenya launched M-Pesa in 2007, the breakthrough that put East Africa on the global map for mobile money. Tanzania followed with Vodacom M-Pesa and Tigo Pesa, expanding steadily through the 2010s. Uganda launched mobile money around 2009. Ethiopia, meanwhile, didn't see its first major mobile money platform until 2021, a full fourteen years behind Kenya.

That gap alone tells most of the story. But it also raises a harder question: why? Part of the answer lies in institutional history. India, for instance, established its Reserve Bank in 1935, passed its Banking Regulation Act in 1949, and computerized its banks through the 1980s, meaning that when the internet arrived, India had banks ready to absorb it. Ethiopia deployed its first ATM in 2001, already fourteen years behind India's 1987 benchmark. Scaling digital infrastructure proved equally difficult: the country struggled against political instability, the legacy of a command economy and the complete absence of a regulatory framework for fintech, a gap that would not begin to close until the 2020s. The lesson here that Ethiopia was never given the institutional runway that other countries quietly benefited from for decades.

2021: The Door Opens

Image from NBE: Comparative table of financial sector assets (% GDP) and number of institutions for Ethiopia and Kenya.

The 2021 NBE directives were a fundamental rewriting of who could participate in Ethiopia's financial system and how.

Before these directives, fintech companies were legally classified as ICT firms, regulated by the Ministry of Innovation and Technology rather than the NBE, and left in a grey zone with no clear path to offering financial services. The new framework changed this completely. For the first time in Ethiopian history, a fintech founder in Addis Ababa didn't need a banking license to build a financial product. Non-bank entities could now legally issue e-wallets, prepaid cards, and mobile money accounts.

The NBE issued its first-ever non-bank mobile money license to Ethio Telecom, enabling the launch of Telebirr. Beyond telecoms, the directives opened the door to fintech startups, microfinance institutions, and non-bank payment gateway operators. Regulatory oversight was consolidated under the NBE, giving the sector legitimacy in the eyes of both investors and users.

The results were swift. Telebirr reached 42 million registered users within its first two years and grew to approximately 54 million by 2025. Products like Michu (Ethiopia's first uncollateralized digital loan by Cooperative Bank of Oromia) and DubeAle (a "Buy Now, Pay Later" scheme by Dashen Bank) emerged almost immediately. The ecosystem began to move.

But there was a major barrier, the sluggish integration of private fintech companies into the broader ecosystem. While new players are emerging, their progress falls well short of expectations and much of that friction is institutional. The approval process is opaque and slow, and the system, in practice, appears to function smoothly only for government-backed entities like Telebirr and state-affiliated payment gateways. Private innovators are largely left to navigate a process that was never designed with them in mind.

I experienced it firsthand while working as a developer at a startup building a payment gateway (a platform that would allow users to send money across wallets without involving traditional banking entities). Getting the license to operate was, to put it plainly, painful. Endless paperwork, cancelled appointments, and layers of bureaucracy consumed time and resources that a lean startup simply cannot afford to waste. Without meaningful reform to this process, it is difficult to imagine how domestic private payment infrastructure will develop or how Ethiopia will ever close the gap with regional peers who have thriving, competitive fintech ecosystems.

The Numbers Are Real But Incomplete

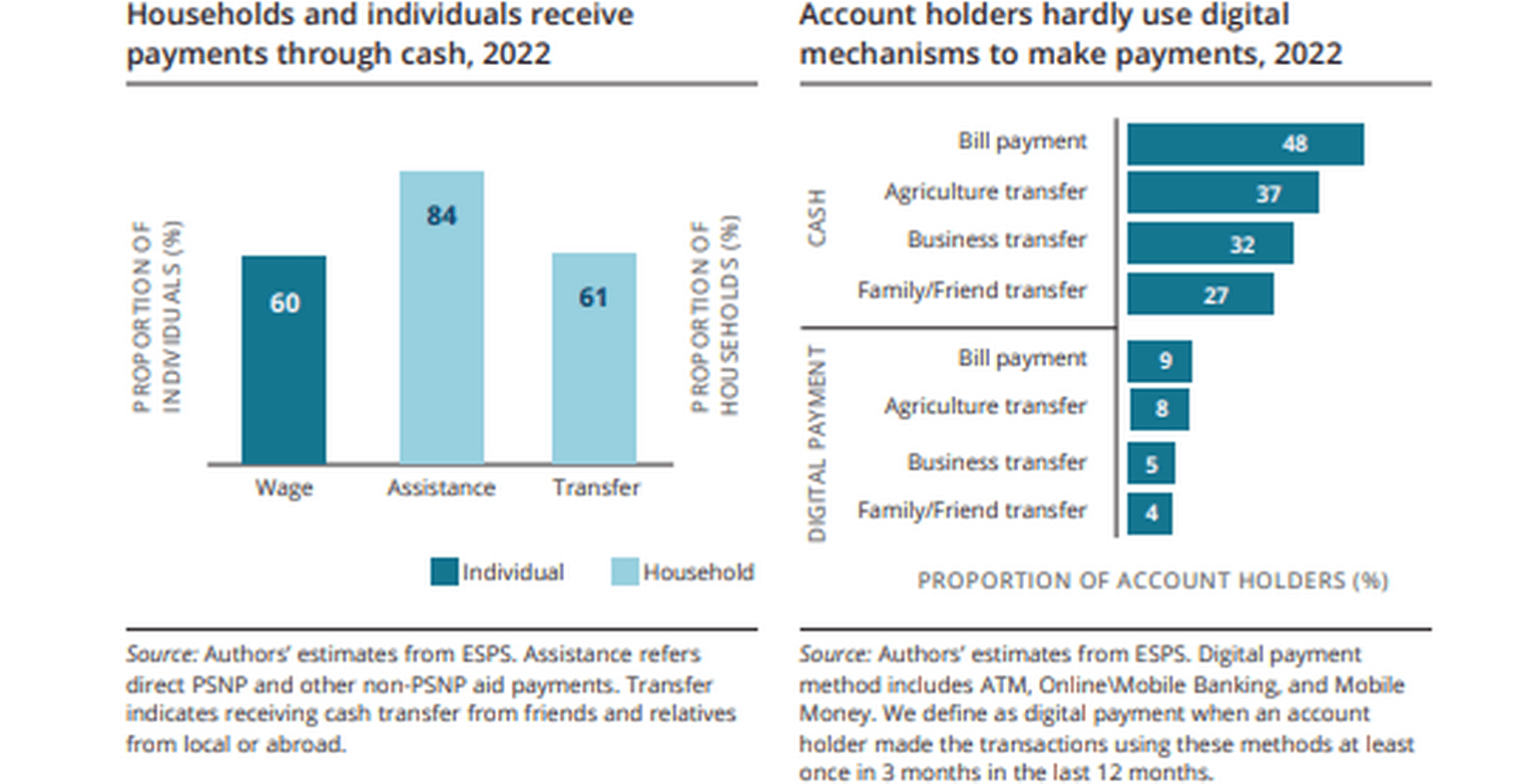

Image: Payment behavior of households and individuals in Ethiopia, 2022. Source: Authors' estimates from the Ethiopian Socioeconomic Survey (ESPS), World Bank.

The headline figures are genuinely impressive. Total digital accounts in Ethiopia more than doubled, from 94.7 million in June 2022 to over 222 million by March 2025. Telebirr processed over 1 trillion Birr in transactions in a single six-month window between September 2024 and February 2025, nearly matching its entire three-year cumulative volume.

But signing up users is the easy part. Getting them to actively and meaningfully use digital finance is where the real challenge lives. There are still market vendors who refuse e-money, mothers who avoid mobile banking and security fears that remain unaddressed. According to the World Bank's Global Findex Database (2021), only 42% of account holders, just 20% of all Ethiopian adults, used their accounts for digital payments in the past year. In Tanzania, that figure stands at 96% of account holders.

The Last-Mile Problem

Several compounding barriers explain why Ethiopia continues to lose people between account creation and active use.

Device and connectivity gaps. Only 58% of Ethiopian adults own any mobile phone as of 2025 and a large share of those are basic feature phones, meaning app-based financial services are entirely out of reach. Internet access follows the same pattern: mobile broadband technically covers 94% of the population geographically, yet only 21–25% of Ethiopians are actual internet users. Ethiopia's median fixed broadband speed sits at just 9.01 Mbps, far behind Rwanda and South Africa where mobile speeds exceed 35 Mbps. Coverage is not the same as connectivity.

Digital and financial literacy. Many Ethiopians, particularly in rural areas where over 70% of the population lives, have no awareness of digital financial services, let alone the confidence to use them. Women face a compounded disadvantage: lower financial literacy, reduced smartphone ownership, and in some regions, cultural barriers that actively discourage independent financial agency.

Trust. A single failed transaction due to a network outage can drive a user permanently back to cash. Fear of losing money through fraud or platform failure keeps many people anchored to community-based systems like the Equb.

Fragmentation. The ecosystem remains siloed. Sending money between platforms: Telebirr to CBE Birr, or to M-Pesa Ethiopia, still requires workarounds. Kenya's M-Pesa became transformative precisely because of its network density and interoperability. Ethiopia is building that connective tissue, but it is not yet in place.

The informal economy. Over 90% of Ethiopia's workforce operates informally, smallholder farmers, street vendors, daily laborers with irregular incomes that don't map onto digital product designs built for formal wage earners. These workers often lack the documentation required for KYC onboarding. The system was not yet designed with them in mind.

What's Still Overdue

Ethiopia has built the regulatory and platform architecture for digital finance. The directives were real. Telebirr is real. The growth numbers are real. But what remains missing is not difficult to identify: limited access to affordable smartphones, weak rural agent networks, fragmented platforms, the absence of a clear data protection framework, and financial products that fail to reflect the realities of an overwhelmingly informal economy. But listing constraints is not enough. The more important question is which change would actually shift the system.

The most immediate lever is standardized API integration. While the National Bank of Ethiopia has already mandated participation in a shared national switch: making basic interoperability a regulatory requirement for licensed payment providers, a formal open-API framework across all licensed providers remains absent. If the NBE were to extend this mandate to API-level integration, the effects would be transformative. Users could move money seamlessly between Telebirr, bank wallets, and emerging fintech platforms beyond the current switch-level connectivity. Merchants could accept payments from any provider through a single interface, and private payment gateways would become fully viable without needing to negotiate access to closed networks.

The deeper effects would follow quickly. Competition would shift away from controlling users toward improving service quality, pricing, and reliability. Transaction costs would fall, making small, everyday payments more viable in digital form. New entrants could build on top of shared infrastructure rather than around it, accelerating innovation across the sector. In that environment, growth would no longer concentrate within a single platform, but distribute across a more open and competitive system, bringing Ethiopia closer to meaningful financial inclusion.

Ethiopia is catching up at a pace that has genuinely surprised analysts, compressing what took Kenya fifteen years into less than five. But catching up in account numbers is not the same as catching up in financial inclusion. The difference between a registered account and a transformed economic life is exactly the distance that the next phase of reform must close.

The door opened in 2021. That much is undeniable.

But for millions of Ethiopians, the experience of walking into a shop, scanning a code, and paying without hesitation, something I once watched as a child still remains just out of reach.

And until that changes, the promise of digital finance in Ethiopia will remain, in every meaningful sense, overdue.

References

Ethiopia’s Economy from an Historical Perspective. Borkena. https://borkena.com/2025/06/03/ethiopias-economy-from-an-historical-perspective/

Mutahi, R. (2025, April 10). Fintech Regulations in Ethiopia: A new era of Digital Finance. https://www.linkedin.com/pulse/fintech-regulations-ethiopia-new-era-digital-finance-robert-mutahi-fn18f

Client challenge. (n.d.). https://www.scribd.com/presentation/936079604/The-Evolution-of-Ethiopias-Financial-System-1

M-Pesa VS Telebirr : The battle for customers as Safaricom Ethiopia granted mobile money license. (n.d.). Garowe Online. https://garoweonline.com/en/featured/business-n/m-pesa-vs-telebirr-the-battle-for-customers-as-safaricom-ethiopia-granted-mobile-money-license

Klapper, L., & Rawlins, M. R. (2024, March 16). Mobile phone technology could expand equitable access to financial services in Ethiopia. World Bank Blogs. https://blogs.worldbank.org/en/africacan/mobile-phone-technology-could-expand-equitable-access-financial-services-ethiopia

I remember watching an Indian movie as a kid, and when I say kid, keep in mind I'm 26 now, so that was probably fifteen or sixteen years ago. In one scene, a character orders food and pays by scanning a QR code and I remember being amazed by it. You might be wondering where I'm going with this, and you're right to pause. But here's the thing: when Telebirr was introduced in 2021, a year after the National Bank of Ethiopia allowed non-bank institutions to provide digital financial services, and we finally started sending and receiving money digitally, I couldn't help but realize just how slowly our system has been catching up with the rest of the world.

According to a 2023 report by DAI Global, before 2017, only 0.3% of Ethiopians held mobile money accounts, an almost invisible figure compared to the Sub-Saharan African average of 21%. The primary bottleneck behind this gap, sustained for years, was a deeply cash-based economy dominated by state-owned financial institutions. Then in 2021, the National Bank of Ethiopia signaled a fundamental shift, opening the door to digital transformation. That same year, Ethio Telecom launched Telebirr, which quickly became the dominant force in the country's digital finance sector. That is what I want to explore in this essay: the rapid rise of digital financial platforms, the structural and institutional barriers that continue to slow them down, the distance that still separates access from true inclusion and the unfulfilled promise of digital financial services in Ethiopia and what it will take for that promise to stop being overdue.

Image from Dai Global: A person making a cash payment at a small kiosk/shop window

A System Built to Exclude

Before 2021, Ethiopia's financial landscape was defined by state dominance, structural underdevelopment, and a population with limited access to or awareness of formal financial services. Ethiopia's modern banking history traces back to 1906, when the Bank of Abyssinia was established as a foreign-owned concession, leaving the country without a single domestic financial institution. That gap was not filled until 1931, when the Bank of Ethiopia was founded under Emperor Haile Selassie. Its growth, however, was cut short by the Italian occupation of 1935–1941, which disrupted the nascent system before it could take root.

After liberation, a modest banking infrastructure began to re-emerge. When the Derg military regime seized power, all private banks were nationalized, plunging the sector into stagnation and contributing to sluggish GDP growth for nearly fifteen years.

The Benchmark: 14 Years Behind

To understand the scale of Ethiopia's delayed start, consider the region. Kenya launched M-Pesa in 2007, the breakthrough that put East Africa on the global map for mobile money. Tanzania followed with Vodacom M-Pesa and Tigo Pesa, expanding steadily through the 2010s. Uganda launched mobile money around 2009. Ethiopia, meanwhile, didn't see its first major mobile money platform until 2021, a full fourteen years behind Kenya.

That gap alone tells most of the story. But it also raises a harder question: why? Part of the answer lies in institutional history. India, for instance, established its Reserve Bank in 1935, passed its Banking Regulation Act in 1949, and computerized its banks through the 1980s, meaning that when the internet arrived, India had banks ready to absorb it. Ethiopia deployed its first ATM in 2001, already fourteen years behind India's 1987 benchmark. Scaling digital infrastructure proved equally difficult: the country struggled against political instability, the legacy of a command economy and the complete absence of a regulatory framework for fintech, a gap that would not begin to close until the 2020s. The lesson here that Ethiopia was never given the institutional runway that other countries quietly benefited from for decades.

2021: The Door Opens

Image from NBE: Comparative table of financial sector assets (% GDP) and number of institutions for Ethiopia and Kenya.

The 2021 NBE directives were a fundamental rewriting of who could participate in Ethiopia's financial system and how.

Before these directives, fintech companies were legally classified as ICT firms, regulated by the Ministry of Innovation and Technology rather than the NBE, and left in a grey zone with no clear path to offering financial services. The new framework changed this completely. For the first time in Ethiopian history, a fintech founder in Addis Ababa didn't need a banking license to build a financial product. Non-bank entities could now legally issue e-wallets, prepaid cards, and mobile money accounts.

The NBE issued its first-ever non-bank mobile money license to Ethio Telecom, enabling the launch of Telebirr. Beyond telecoms, the directives opened the door to fintech startups, microfinance institutions, and non-bank payment gateway operators. Regulatory oversight was consolidated under the NBE, giving the sector legitimacy in the eyes of both investors and users.

The results were swift. Telebirr reached 42 million registered users within its first two years and grew to approximately 54 million by 2025. Products like Michu (Ethiopia's first uncollateralized digital loan by Cooperative Bank of Oromia) and DubeAle (a "Buy Now, Pay Later" scheme by Dashen Bank) emerged almost immediately. The ecosystem began to move.

But there was a major barrier, the sluggish integration of private fintech companies into the broader ecosystem. While new players are emerging, their progress falls well short of expectations and much of that friction is institutional. The approval process is opaque and slow, and the system, in practice, appears to function smoothly only for government-backed entities like Telebirr and state-affiliated payment gateways. Private innovators are largely left to navigate a process that was never designed with them in mind.

I experienced it firsthand while working as a developer at a startup building a payment gateway (a platform that would allow users to send money across wallets without involving traditional banking entities). Getting the license to operate was, to put it plainly, painful. Endless paperwork, cancelled appointments, and layers of bureaucracy consumed time and resources that a lean startup simply cannot afford to waste. Without meaningful reform to this process, it is difficult to imagine how domestic private payment infrastructure will develop or how Ethiopia will ever close the gap with regional peers who have thriving, competitive fintech ecosystems.

The Numbers Are Real But Incomplete

Image: Payment behavior of households and individuals in Ethiopia, 2022. Source: Authors' estimates from the Ethiopian Socioeconomic Survey (ESPS), World Bank.

The headline figures are genuinely impressive. Total digital accounts in Ethiopia more than doubled, from 94.7 million in June 2022 to over 222 million by March 2025. Telebirr processed over 1 trillion Birr in transactions in a single six-month window between September 2024 and February 2025, nearly matching its entire three-year cumulative volume.

But signing up users is the easy part. Getting them to actively and meaningfully use digital finance is where the real challenge lives. There are still market vendors who refuse e-money, mothers who avoid mobile banking and security fears that remain unaddressed. According to the World Bank's Global Findex Database (2021), only 42% of account holders, just 20% of all Ethiopian adults, used their accounts for digital payments in the past year. In Tanzania, that figure stands at 96% of account holders.

The Last-Mile Problem

Several compounding barriers explain why Ethiopia continues to lose people between account creation and active use.

Device and connectivity gaps. Only 58% of Ethiopian adults own any mobile phone as of 2025 and a large share of those are basic feature phones, meaning app-based financial services are entirely out of reach. Internet access follows the same pattern: mobile broadband technically covers 94% of the population geographically, yet only 21–25% of Ethiopians are actual internet users. Ethiopia's median fixed broadband speed sits at just 9.01 Mbps, far behind Rwanda and South Africa where mobile speeds exceed 35 Mbps. Coverage is not the same as connectivity.

Digital and financial literacy. Many Ethiopians, particularly in rural areas where over 70% of the population lives, have no awareness of digital financial services, let alone the confidence to use them. Women face a compounded disadvantage: lower financial literacy, reduced smartphone ownership, and in some regions, cultural barriers that actively discourage independent financial agency.

Trust. A single failed transaction due to a network outage can drive a user permanently back to cash. Fear of losing money through fraud or platform failure keeps many people anchored to community-based systems like the Equb.

Fragmentation. The ecosystem remains siloed. Sending money between platforms: Telebirr to CBE Birr, or to M-Pesa Ethiopia, still requires workarounds. Kenya's M-Pesa became transformative precisely because of its network density and interoperability. Ethiopia is building that connective tissue, but it is not yet in place.

The informal economy. Over 90% of Ethiopia's workforce operates informally, smallholder farmers, street vendors, daily laborers with irregular incomes that don't map onto digital product designs built for formal wage earners. These workers often lack the documentation required for KYC onboarding. The system was not yet designed with them in mind.

What's Still Overdue

Ethiopia has built the regulatory and platform architecture for digital finance. The directives were real. Telebirr is real. The growth numbers are real. But what remains missing is not difficult to identify: limited access to affordable smartphones, weak rural agent networks, fragmented platforms, the absence of a clear data protection framework, and financial products that fail to reflect the realities of an overwhelmingly informal economy. But listing constraints is not enough. The more important question is which change would actually shift the system.

The most immediate lever is standardized API integration. While the National Bank of Ethiopia has already mandated participation in a shared national switch: making basic interoperability a regulatory requirement for licensed payment providers, a formal open-API framework across all licensed providers remains absent. If the NBE were to extend this mandate to API-level integration, the effects would be transformative. Users could move money seamlessly between Telebirr, bank wallets, and emerging fintech platforms beyond the current switch-level connectivity. Merchants could accept payments from any provider through a single interface, and private payment gateways would become fully viable without needing to negotiate access to closed networks.

The deeper effects would follow quickly. Competition would shift away from controlling users toward improving service quality, pricing, and reliability. Transaction costs would fall, making small, everyday payments more viable in digital form. New entrants could build on top of shared infrastructure rather than around it, accelerating innovation across the sector. In that environment, growth would no longer concentrate within a single platform, but distribute across a more open and competitive system, bringing Ethiopia closer to meaningful financial inclusion.

Ethiopia is catching up at a pace that has genuinely surprised analysts, compressing what took Kenya fifteen years into less than five. But catching up in account numbers is not the same as catching up in financial inclusion. The difference between a registered account and a transformed economic life is exactly the distance that the next phase of reform must close.

The door opened in 2021. That much is undeniable.

But for millions of Ethiopians, the experience of walking into a shop, scanning a code, and paying without hesitation, something I once watched as a child still remains just out of reach.

And until that changes, the promise of digital finance in Ethiopia will remain, in every meaningful sense, overdue.

References

Ethiopia’s Economy from an Historical Perspective. Borkena. https://borkena.com/2025/06/03/ethiopias-economy-from-an-historical-perspective/

Mutahi, R. (2025, April 10). Fintech Regulations in Ethiopia: A new era of Digital Finance. https://www.linkedin.com/pulse/fintech-regulations-ethiopia-new-era-digital-finance-robert-mutahi-fn18f

Client challenge. (n.d.). https://www.scribd.com/presentation/936079604/The-Evolution-of-Ethiopias-Financial-System-1

M-Pesa VS Telebirr : The battle for customers as Safaricom Ethiopia granted mobile money license. (n.d.). Garowe Online. https://garoweonline.com/en/featured/business-n/m-pesa-vs-telebirr-the-battle-for-customers-as-safaricom-ethiopia-granted-mobile-money-license

Klapper, L., & Rawlins, M. R. (2024, March 16). Mobile phone technology could expand equitable access to financial services in Ethiopia. World Bank Blogs. https://blogs.worldbank.org/en/africacan/mobile-phone-technology-could-expand-equitable-access-financial-services-ethiopia

Back to Top